Understanding retirement plan fee changes

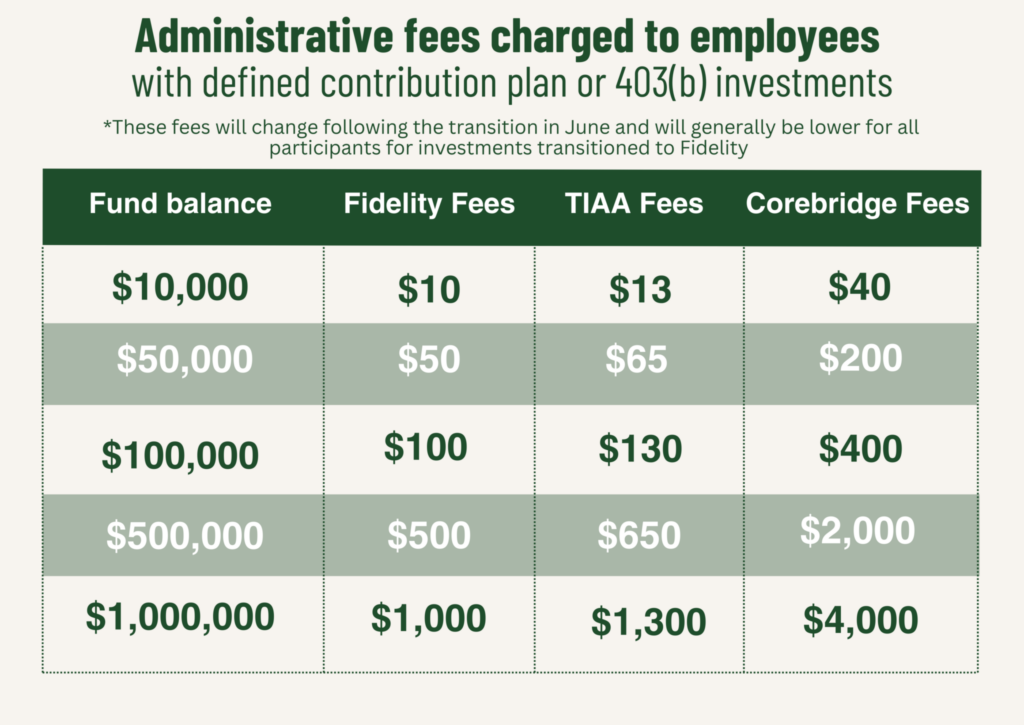

Administrative Fees

- Administrative fees are paid to the company that is the retirement plan service provider to manage your plan and keep records of your investments. Previously, those companies were TIAA, Corebridge and Fidelity.

- CSU has negotiated a fixed fee with Fidelity for each participant. Previously, you may have been charged for each type of CSU retirement investment you had; if you had investments in both a DCP and a 403(b), you were charged two separate fees.

- We are in the process of determining how many accounts will transfer to Fidelity from Corebridge and TIAA. Then Fidelty fees will be shared equitably across participants.

- You will pay one fixed fee if you are enrolled in the DCP, 403(b) or both under this model.

- Currently you pay a fee for each account under Fidelity, TIAA or Corebridge.

Investment Fees

- You currently pay investment fees to TIAA, Corebridge or Fidelty to manage your retirement fund.

- These fees are based on a percentage of assets you have in an investment fund. These are disclosed in the fund prospectus.

- Fees are deducted from your investment balance through an indirect charge against your account.

- Your net total return is your return after these fees have been deducted.

- The new core fund line-up selected by the CSU Retirement Investment Committee chose best in class funds with competitive performance and investment fees.

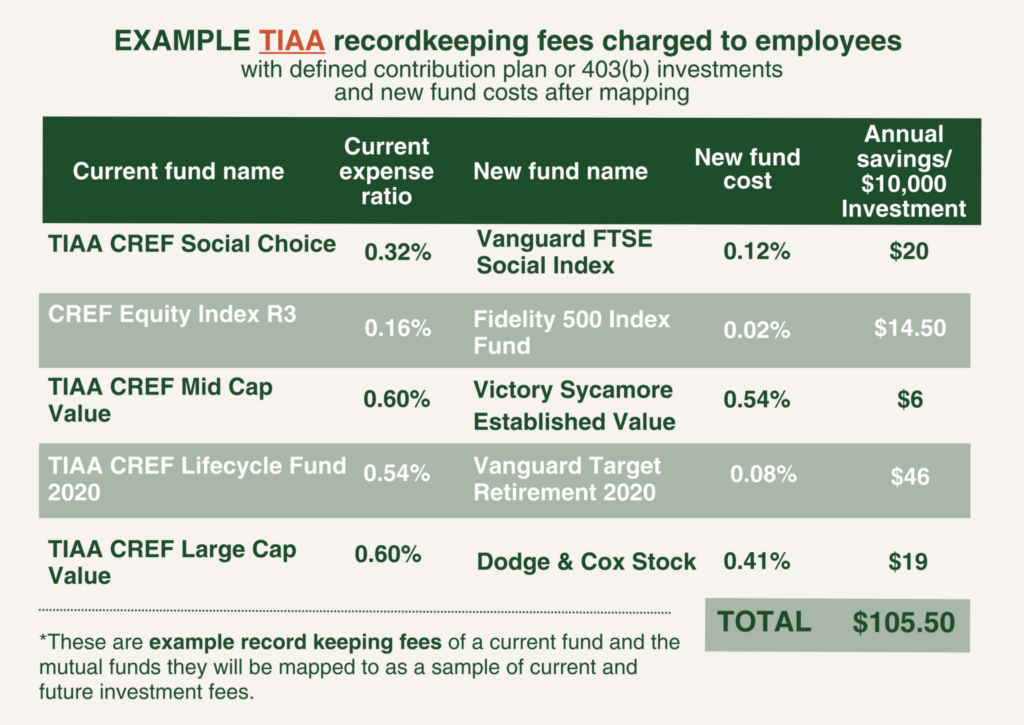

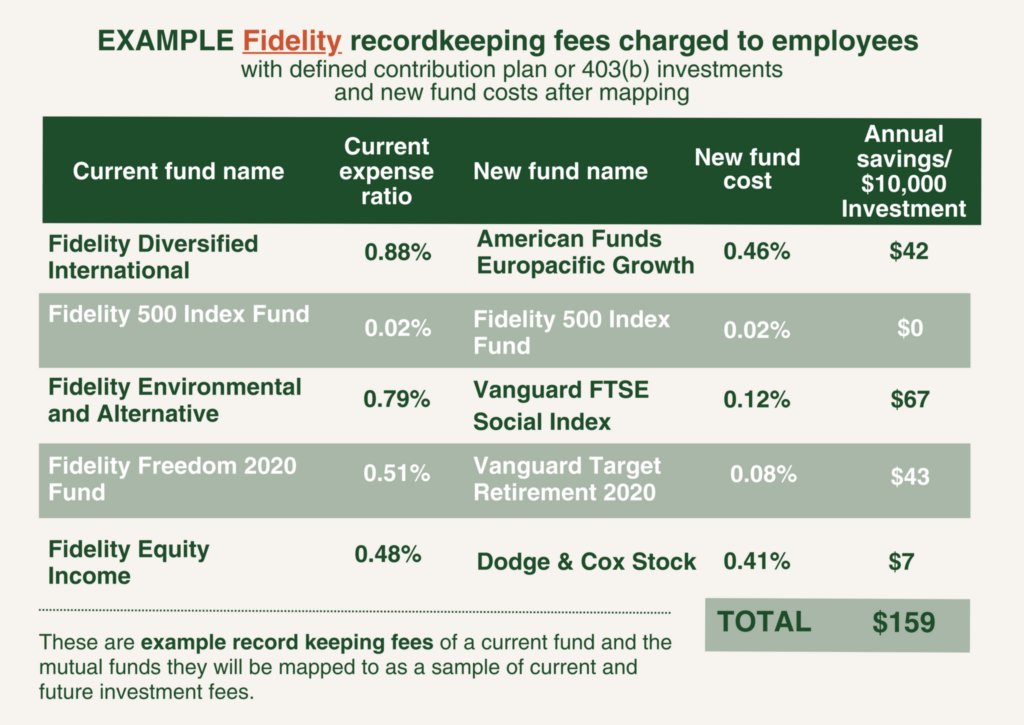

Below are examples of how fees will change under the new structure. Because investment fees are based on a percentage of assets, these are examples only but show a comparison of current investment fees to investment fees after the transition.